The Complete Guide to Private Mortgages (Part 1)

*This post is sponsored by one of The Real Estate Investment Network’s Trusted Partners, Private Money 4 Mortgages. To become a contributing editor or to learn about our sponsorship opportunities, please contact us at david@reincanada.com.

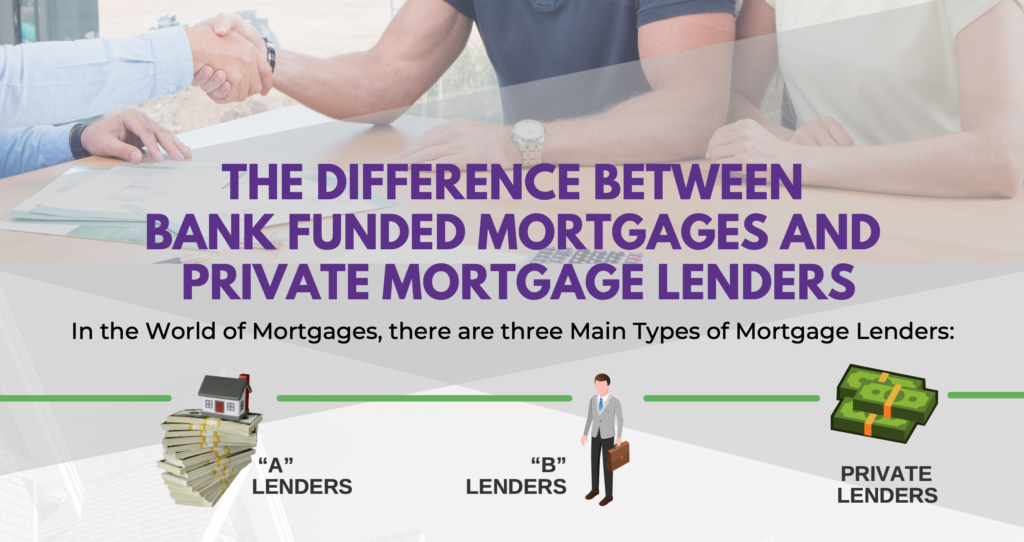

First, let’s define what is a private mortgage?

Simply put, this is a mortgage that is NOT funded through a bank or financial institution. Private mortgage lenders are private corporations, individuals, or groups of individuals who lend out their own money. This includes Mortgage Investment Corporations (MIC), where money from private investors is pooled to fund syndicated mortgages.

Private mortgages are typically shorter term and come with higher interest rates and fees as opposed to mortgages offered by traditional financial institutions. They are meant to be a temporary measure before transitioning back to typical mortgage lenders.

The “A” lenders consist of the traditional banks and institutions that most people bank with. These lenders are usually the first choice for borrowers who seek a mortgage approval. There are also “Alternative A” mortgage lenders who offer products very competitively to that of banks and are often able to provide better rates. These institutions usually operate as “Monoline lenders” which basically means that they only deal in one area of banking and do not offer full services as the five major banks do.

Approval by these “A” lenders is very strict, and therefore the applicant must demonstrate low risk, great credit and provable tenured income. Most of these types of mortgages are also insured to protect the interests of these banks and institutions. Since the respective insurance companies are in the business of maximizing the collection of premiums and minimizing claims, they too are looking for low-risk applicants.

The “B” lenders consist of various non-banking institutions that deal almost exclusively in mortgages. Unlike the “A” lenders, these types of lenders are not as strict when it comes to their mortgage approval guidelines. Therefore, clients with marginal credit scores and low income can still get approved for a mortgage.

Having said that though, these mortgage products require a down payment of at least 20%, because most “B” lenders only provide uninsured mortgages up to 80% of the purchase price. These lenders will take on higher applicant risk and therefore their mortgage products have higher interest rates than those offered by “A” Lenders.

Private mortgage lenders are typically the equity based lenders. This means that these lenders are more interested in the available equity of the home, than they are of the applicants’ income and credit score. They will apply a very “common sense” approach to the qualifying process of the borrower and their situation. The three main things that a Private Lender looks at are

a) the story as to why a private mortgage is needed,

b) the details of the property and

c) the exit strategy in order to get out of this short term loan. Since a Private lender is usually a last resort, the cost is significantly higher than banks and other mortgage institutions.

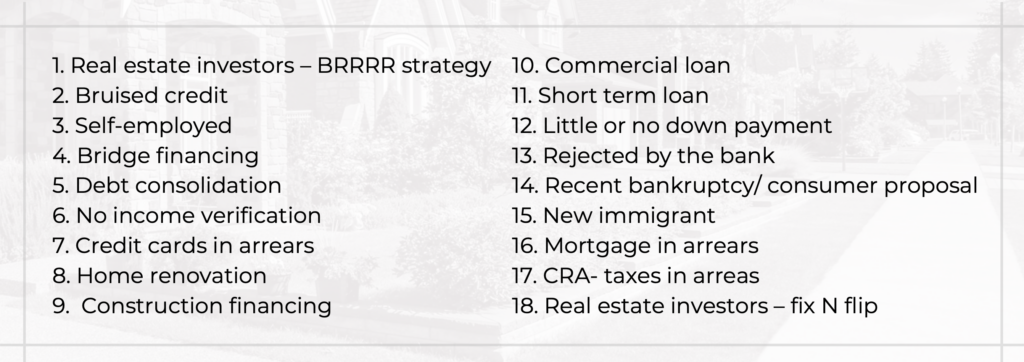

Why Would Someone Need a Private Mortgage?

There are many situations that will prevent someone from qualifying with a bank or financial institution when looking for a mortgage. Below are many examples of why it might be necessary to get financed through a private lender:

In many of the above examples, you would start with a short term private mortgage and then once your situation has improved, you can then refinance with an institutional lender. In Part 2, we’ll dive into situations where real estate investors might need a second mortgage and why real estate investors often use them.

All Access

")

")